Today, June 30, is the reference date for calendar year-end companies to calculate next year’s filer status, as well as the aggregate market value of equity held by non-affiliates (i.e., public float) for purposes of inclusion in the annual report on Form 10-K to be filed in early 2021. In preparing these calculations, it is important each year for counsel to apply the definitions of public float and the relevant filer statuses to ensure that upcoming filings are made timely.

For calculating 2021 filer status, however, several of the definitions have changed. Earlier this year, the SEC adopted amendments adding a revenue element to the definitions of accelerated filer and large accelerated filer to exclude low revenue filers. While relatively straightforward in theory, the tests have proven rather complicated in practice. To assist companies in applying the amendments, the SEC has produced a Small Entity Compliance Guide. Although helpful, even this guide may prove difficult at times to follow.

Since most companies will start analyzing these changes today, this blog post is intended as a practical reminder of and gap-filling guide to the relevant changes for public companies. Generally, the amended definitions now include a carve-out for smaller reporting companies (SRC) with annual revenues less than $100 million in most recent audited annual financial statements.

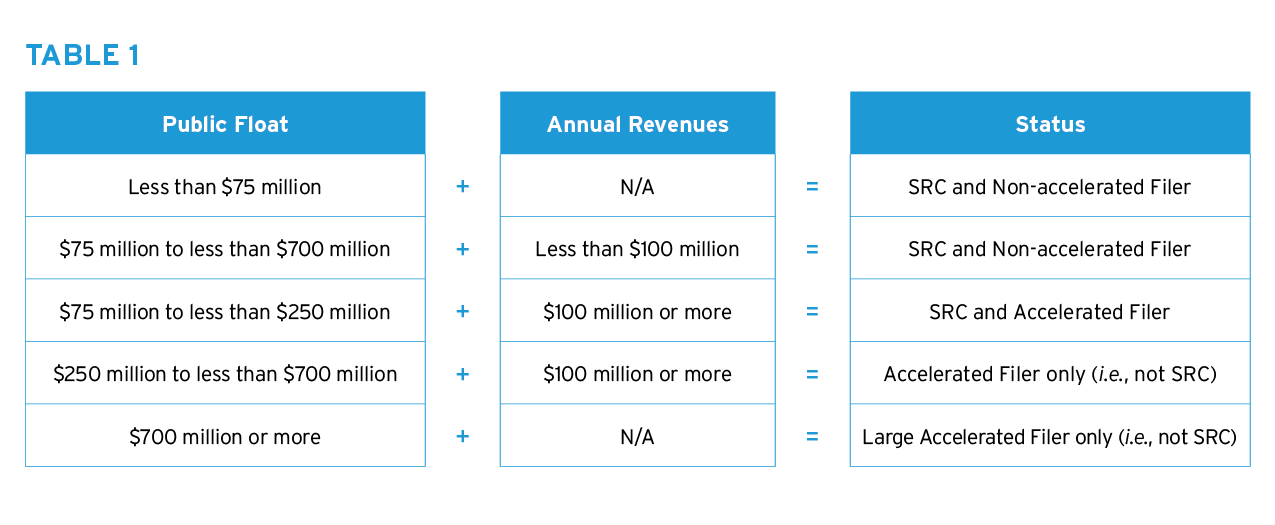

Public Float and Annual Revenue Requirements

The public float and annual revenue requirements are included in Table 1 below. A company’s status can be determined by using public float and annual revenue numbers to work from left to right across a row in Table 1. For example, a company with a public float of $215 million and $110 million in annual revenue would fall into the third row of Table 1, qualifying as an SRC and accelerated filer. Public float is calculated according to the requirements and instructions of Rule 12b-2 and consistent with prior year calculations, and generally includes all outstanding common stock not held by an insider (eg, officers and directors). Annual revenues should equal the number used in the company’s most recent audited annual financial statements.

Amended Transition Thresholds

In addition, the amendments increased the transition thresholds, which potentially permits companies previously at the bottom edge of a filer status range to transition to the more lenient, lower filer status. Significantly complicating the transition calculations, however, the SEC also amended the SRC transition thresholds to include a revenue component, and specifically excluded a transitioned SRC from the definitions of accelerated filer and large accelerated filer. Sound confusing? It is, and the complexity of the new rule was one of its foremost criticisms.

Requalification as a “Smaller Reporting Company”

In short, a company that did not previously qualify as an SRC may be able to requalify under the smaller reporting company definition of Rule 12b-2. Upon requalification, the SRC would become a non-accelerated filer (i.e., not an accelerated or large accelerated filer) regardless of the other transition rules. As the SEC’s adopting release explained, under the amendments “an accelerated filer would remain an accelerated filer until its public float falls below $60 million or its annual revenues fall below the applicable revenue threshold ($80 million or $100 million), at which point it would become a non-accelerated filer,” and similar rules apply for large accelerated filers.

More concretely, under the amended rules, a company can requalify as an SRC, and thereby as a non-accelerated filer, if either of the following is true:

- Its public float is less than $200 million, or

- Its public float and its annual revenues meet the requirements of the following Table 2.

For today’s calculation and Table 2, a calendar-year company should reference the prior public float as of June 30, 2019, and the prior annual revenues listed in the 2018 audited annual financial statements.

Determining Public Float for Non-SRCs

If a company is not an SRC under Table 2, then it is necessary to proceed to the next step of reviewing the other amended transition thresholds for accelerated filers and large accelerated filers (see Table 3, with the amended thresholds emphasized).

Again, Table 3 should only be referenced for a non-SRC to determine whether it is moving down a filer status level, while Table 1 should be referenced to determine if a company is moving up to a higher filer status.

Practitioners and counsel for dual-status companies, in particular, would be well advised to read these changes closely and calculate carefully.

If you have any questions about the joint statement or in general, please feel free to email the author directly or, if applicable, contact your primary Bass, Berry & Sims relationship attorney.

About the Bass, Berry & Sims Corporate & Securities Practice

Public and private companies of all sizes across a variety of industries turn to Bass, Berry & Sims for counsel on a wide range of corporate matters, including mergers, acquisitions and dispositions; capital markets transactions; executive compensation issues; corporate governance; and shareholder activism. We serve as primary corporate and securities counsel to more than 35 public companies and have counseled on 150 deals ranging in size from $20 million to more than $15 billion over the past two years. Click here to learn more about the Corporate & Securities Practice at Bass, Berry & Sims.